December 01, 2025

How To Decide Between Investment Loans And Working Capital Loans For Growth

Investment Loan vs. Working Capital Loan: Which To Choose For Growth

Every business reaches moments when internal funds are not enough. Whether to seize an opportunity or to stay afloat during a seasonal dip, financing becomes essential. Yet not all loans serve the same purpose. Investment loans and working capital loans may look similar on paper—both provide cash—but their functions diverge sharply. Understanding these differences is crucial for entrepreneurs deciding how to fuel growth without creating hidden risks. Choosing the wrong type can turn a manageable obligation into a structural weakness. Choosing correctly can position a business for stability and expansion at the same time.

Why The Distinction Between Loan Types Matters

Confusing investment loans with working capital loans is one of the most common mistakes in business financing. Each loan is designed for a different horizon, with repayment terms, interest rates, and expectations that match distinct needs. An investment loan finances long-term assets—machines, property, or technology—that will generate returns over years. A working capital loan, by contrast, covers short-term needs such as payroll, inventory, or temporary cash shortages. Using one in place of the other creates mismatched obligations. A company funding day-to-day expenses with a 10-year investment loan risks unnecessary costs, while financing long-term assets with short-term credit creates liquidity crises. Clarity ensures that debt strengthens rather than destabilizes the enterprise.

What Is An Investment Loan?

An investment loan is designed for long-term projects that increase productive capacity or efficiency. Companies borrow to purchase equipment, build new facilities, or develop large-scale technology systems. Repayment schedules are usually spread over several years, often with fixed installments that match the expected life of the asset. Interest rates may be lower than short-term loans because collateral is tangible and predictable. The central feature is alignment: long-term capital for long-term returns. Businesses using investment loans must be certain that the asset will generate sufficient revenue to cover repayments, since these loans cannot be repaid by short-term sales cycles alone.

When To Use An Investment Loan

Firms turn to investment loans when they are ready to scale sustainably. Examples include a manufacturer purchasing new assembly lines, a logistics company building a distribution center, or a retailer acquiring property for expansion. The critical element is permanence: the asset financed should provide value for many years. Entrepreneurs must also prepare detailed forecasts, since lenders scrutinize repayment capacity over long horizons. The wrong use—such as covering temporary shortages with investment loans—locks businesses into debt without corresponding long-term benefits.

What Is A Working Capital Loan?

Unlike investment loans, working capital loans serve immediate, short-term needs. They provide liquidity to cover payroll, rent, supplier payments, or seasonal inventory buildup. These loans usually have shorter repayment terms, often less than two years, and may come with higher interest rates. Instead of funding new assets, they stabilize operations. Working capital loans are especially valuable in industries with strong seasonality, where revenues fluctuate but expenses remain constant. They act as a bridge between income and obligations, ensuring continuity without forcing businesses to cut corners or delay payments.

When To Use A Working Capital Loan

Working capital loans make sense when temporary imbalances threaten stability. A retailer stocking up for holiday demand, a farmer covering costs until harvest sales arrive, or a consultancy bridging delays in client payments all benefit from this tool. The defining feature is short duration. These loans should not finance permanent investments because the repayment horizon is too narrow. If a company buys machinery with working capital credit, it may face repayment pressure before the asset produces sufficient returns. Using them responsibly means recognizing their role as stabilizers, not engines of long-term growth.

| Feature | Investment Loan | Working Capital Loan |

|---|---|---|

| Purpose | Long-term assets and expansion projects | Short-term operational expenses |

| Repayment Term | 3–15 years | 3–24 months |

| Collateral | Property, equipment, or other fixed assets | Receivables, inventory, or unsecured |

| Interest Rate | Generally lower due to collateral security | Higher due to short duration and risk |

| Best Use | Scaling production, facility construction | Payroll, seasonal purchases, bridging receivables |

How To Decide Which Loan Supports Growth

The choice between investment and working capital loans hinges on business goals. If the objective is to expand capacity or enter new markets, investment loans provide the stability needed for large expenditures. If the goal is to stabilize cash flow during fluctuations, working capital loans prevent disruption. Growth requires both types at different stages. A balanced financing strategy recognizes that immediate stability must support long-term expansion. One without the other creates vulnerabilities—expansion collapses without liquidity, and liquidity becomes meaningless without growth.

Risks Of Misusing Each Loan Type

Misalignment between loan type and purpose creates risks that can erode growth. Funding payroll with long-term loans may lead to ongoing dependence, since no new income stream emerges to repay debt. Using short-term loans for major projects creates repayment stress, often forcing refinancing at unfavorable rates. Both errors transform credit from a tool into a liability. Businesses must therefore discipline themselves to match loan duration with the economic life of the financed need. Responsible borrowing means aligning purpose, timing, and repayment with strategic objectives.

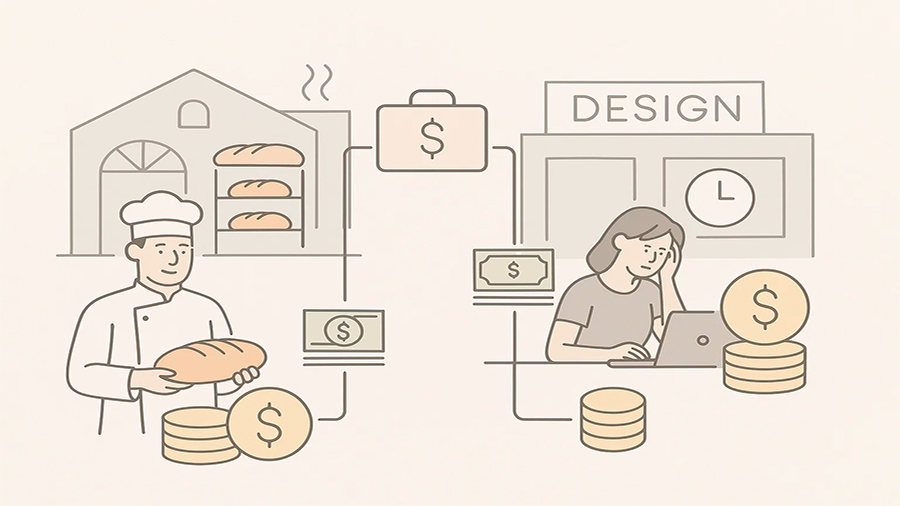

Examples From Real Business Scenarios

Consider two companies facing different challenges. A bakery chain decides to open a new central kitchen to serve multiple locations. The project requires significant upfront costs but will reduce per-unit production expenses over a decade. Here, an investment loan aligns perfectly. Contrast this with a design agency that experiences late payments from clients but must still cover staff salaries. A working capital loan provides immediate liquidity until receivables are collected. If either company swapped loan types, the bakery would face repayment deadlines before profits materialized, while the agency would carry long-term debt for short-term needs. Both would weaken their positions instead of strengthening them.

Factors That Influence Loan Choice Beyond Purpose

Purpose is the primary distinction, but other factors shape decisions. Interest rate environments affect affordability. A period of low rates may encourage longer-term borrowing for expansion, while high rates make short-term loans more attractive. Collateral availability also plays a role: firms with strong fixed assets can access investment loans more easily, while asset-light businesses rely on working capital credit. Finally, the business cycle matters. During growth periods, investment loans support expansion. During downturns, working capital loans preserve continuity. Recognizing these dynamics ensures that borrowing decisions are adapted to context rather than made mechanically.

How Lenders Evaluate Loan Applications

Lenders differentiate between the two loan types as carefully as businesses should. For investment loans, they evaluate project feasibility, expected returns, and collateral value. For working capital loans, they study receivables, sales cycles, and operational efficiency. A company applying for the wrong loan type may face rejection not because of weakness but because of mismatch. Entrepreneurs who understand lender expectations can present stronger applications. They can also negotiate better terms by aligning requests with the institution’s risk assessment framework. Awareness of this perspective prevents wasted effort and increases approval chances.

Balancing Both Loan Types In Growth Strategy

In practice, most growing businesses use both loan types at different times. Investment loans provide the backbone of expansion—factories, fleets, or property. Working capital loans keep day-to-day operations stable during growth. Combining both allows firms to scale without losing momentum. The balance depends on industry dynamics. A construction firm may rely more heavily on working capital loans to manage project cycles, while a technology company emphasizes investment loans for product development. Successful growth comes from treating these tools as complementary rather than mutually exclusive.

The Conclusion

Choosing between investment loans and working capital loans is not about which is better, but about which is appropriate for the moment. Each serves a distinct role: one fuels long-term growth, the other ensures immediate stability. Misusing either creates risks that undermine objectives. By aligning loan type with business purpose, leaders turn debt into leverage rather than liability. Growth depends not only on access to credit but on the wisdom to use the right form at the right time. The companies that master this balance transform borrowing from a necessity into a strategic advantage.